How Much Do You Need To Earn To Comfortably Afford A Landed Home In Singapore (2025)

When people ask “How much do I need to earn to afford a landed property in Singapore?”, the answer isn’t as straightforward as throwing out a single number. Landed homes come in all shapes, sizes. For this article, we’re going to keep things simple and focus on the most accessible category: terrace houses.

Related: All The Different Types Of Landed Homes In Singapore (Terrace, Semi-D, Bungalow, GCB)

Terrace houses are considered entry-level landed because they are the most abundant in terms of supply and also in terms of price.

In this article, we’ll look at what’s currently the cheapest landed property in Singapore (both leasehold and freehold), break down what they’ll actually cost you, and calculate how much income you’d realistically need to buy one without living on instant noodles for the next 30 years.

Landed Homes Mortgage And Monthly Repayment Breakdown (2025)

Here’s how the numbers stack up for an entry-level terrace home in 2025.

Assuming:

Property type: Terrace house

• Price: $3,000,000

• Loan-to-Value (LTV): 75%

• Loan tenure: 30 years

• Interest rate: 3.5% p.a. (stress-tested, in line with MAS guidelines)

• TDSR cap: 55% of gross monthly income

| Item | Amount | Notes |

|---|---|---|

| Purchase price | $3,000,000 | |

| Downpayment (25%) | $750,000 | Cash + CPF |

| Loan amount (75%) | $2,250,000 | |

| Buyer’s Stamp Duty (BSD) | ~$119,600 | Progressive residential rates |

| Legal fees & misc. | ~$5,000 | Varies by law firm |

| Total upfront cost | ~$874,600 | Downpayment + BSD + legal fees |

Monthly Repayments

At 3.5% interest over 30 years for a $2.25M loan:

~$10,100/month in mortgage repayments.

Minimum Household Income Required

With TDSR capped at 55%, your gross monthly household income would need to be around:

$18,364/month to qualify for the above loan.

Pro Tip: The rule of thumb is that for every $1M in loan principal at 3.5% over 30 years works out to roughly $4,480/month in repayments.

Reality Check:

The figures above assume a best-case scenario. 75% Loan-to-Value (LTV) and a full 30-year loan tenure. In reality, the most common factor reducing affordability is borrower’s age:

If the average age between co-borrowers is higher, your maximum loan tenure shrinks, which pushes monthly repayments up.

For example, a 50-year-old buyer might only get a 15-year loan — almost doubling the monthly repayment compared to a 30-year loan.

Income stability, and lender policy can also tighten approval limits, even if you meet MAS guidelines.

In short, use these numbers as a baseline, but expect your actual affordability to be lower if you’re not in the “young, no other housing loans, stable income” bracket.

Cheapest Leasehold Landed Property In Singapore (as of writing)

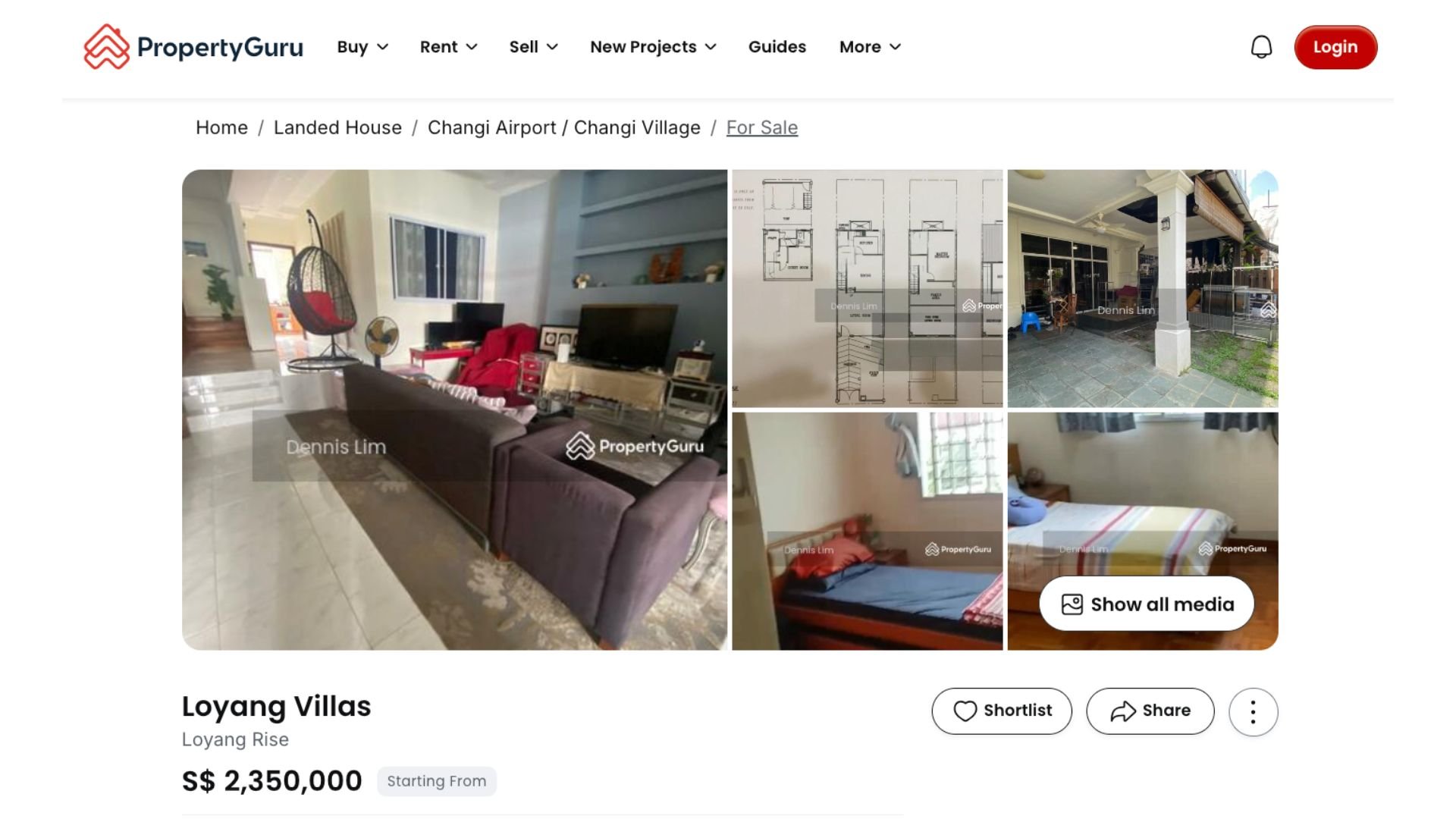

Loyang Villas – Loyang Rise

Price: $2,350,000 (99-year leasehold)

Type: Terrace house

Size: 1,750 sqft built-up

Layout: 5 bedrooms, 5 bathrooms

TOP: December 1997 (≈ 71 years of lease remaining)

Location: 12 min walk to Pasir Ris East MRT (CR4)

| Item | Amount | Notes |

|---|---|---|

| Purchase Price | S$2,350,000 | 99‑year leasehold, ~71 years left |

| Downpayment (25%) | S$587,500 | Cash + CPF |

| Loan Amount (75%) | S$1,762,500 | 30‑year tenure (illustrative) |

| Buyer’s Stamp Duty (BSD) | ~S$87,100 | Progressive residential rates |

| Legal & Misc. Fees | ~S$5,000 | Varies by law firm |

| Total Upfront Cost | ~S$679,600 | Downpayment + BSD + legal fees |

Monthly Repayment (3.5% p.a., 30 years): ~$7,900/month

Minimum Household Income Required (TDSR 55%): ~$14,364/month

This Loyang Villas unit is one of the cheapest landed options in Singapore as of writing, and for good reason:

It’s a 99-year leasehold with ~71 years remaining, which means its financing and resale appeal will diminish further as the lease runs down.

Located in the far east, it offers space and a landed address at a fraction of central Singapore prices, but commute times to the city are long.

The interior and exterior are functional but dated, buyers should budget for upgrades if they want a more modern look.

It’s a lifestyle purchase for those who value space over long-term capital appreciation, and are comfortable with the location and lease profile.

Cheapest Freehold Landed In Singapore (as of writing)

MacPherson Garden Estate – Jalan Gembira

Price: $2,480,000 (Freehold)

Type: Terrace house

Size: 987 sqft land area / 1,200 sqft floor area

Layout: 3 bedrooms, 2 bathrooms

Location: 13 min walk to Mattar MRT (DT25) — central-east city fringe

| Item | Amount | Notes |

|---|---|---|

| Purchase Price | S$2,480,000 | Freehold |

| Downpayment (25%) | S$620,000 | Cash + CPF |

| Loan Amount (75%) | S$1,860,000 | 30-year tenure (illustrative) |

| Buyer’s Stamp Duty (BSD) | ~S$93,800 | Progressive residential rates |

| Legal & Misc. Fees | ~S$5,000 | Varies by law firm |

| Total Upfront Cost | ~S$718,800 | Downpayment + BSD + legal fees |

Monthly Repayment (3.5% p.a., 30 years): ~$8,340/month

Minimum Household Income Required (TDSR 55%): ~$15,164/month

For an extra ~$130K over the Loyang leasehold, this property gives you freehold tenure and a far more central location. On paper, that’s a big win for long-term value retention.

However, the trade-off here is condition — this MacPherson unit is in considerably worse shape than the Loyang house. Buyers should budget for extensive A&A works (Additions & Alterations) or even a full rebuild, both of which can easily push your total spend into the $3M+ range.

That said, once modernised, a well-located freehold terrace in the city fringe is likely to hold or grow in value over time, while the Loyang leasehold will face depreciation pressure as its lease runs down.

Related: What it really cost to rebuild a landed home in Singapore (2025)

How Much You Need To Earn To Buy Brand New Landed Home (2025)

The Harbour Residences – Pasir Panjang Road

• Price: $5,800,000 (Freehold)

• Type: Terrace house

• Size: 1,990 sqft built-up

• Layout: 5 bedrooms, 5 bathrooms

• Location: 7 min walk to Haw Par Villa MRT (CC25) — west coast city fringe

• TOP: September 2026 (brand new, direct from developer)

| Item | Amount | Notes |

|---|---|---|

| Purchase Price | S$5,800,000 | Freehold, brand new |

| Downpayment (25%) | S$1,450,000 | Cash + CPF |

| Loan Amount (75%) | S$4,350,000 | 30‑year tenure (illustrative) |

| Buyer’s Stamp Duty (BSD) | ~S$287,600 | Progressive residential rates |

| Legal & Misc. Fees | ~S$5,000 | Varies by law firm |

| Total Upfront Cost | ~S$1,742,600 | Downpayment + BSD + legal fees |

Monthly Repayment (3.5% p.a., 30 years): ~$19,480/month

Minimum Household Income Required (TDSR 55%): ~$35,418/month

This Harbour Residences unit is everything the cheapest landed examples are not — brand new, tastefully designed, and fitted with the latest floor plan trends and finishes.

For buyers at this level, the appeal is turnkey convenience:

• No renovation downtime or cost overruns.

• Modern layout with large communal spaces, ensuite bedrooms, and integrated storage.

• Structural warranty and developer after-sales support.

The price point puts it far above the “affordable” bracket, but it’s an important benchmark for what the top end of terrace living looks like in Singapore today — and a reminder that for some buyers, time saved is worth more than money saved.

In A Nutshell:

| Property | Tenure | Price | Total Upfront Cost | Est. Monthly Repayment (3.5% p.a., 30 yrs) |

Min. Household Income (TDSR 55%) |

|---|---|---|---|---|---|

| Loyang Villas Far East, 1997 TOP |

99-year leasehold (~71 yrs left) | S$2,350,000 | ~S$679,600 | ~S$7,900 | ~S$14,364 |

| MacPherson Garden Estate City Fringe, Freehold |

Freehold | S$2,480,000 | ~S$718,800 | ~S$8,340 | ~S$15,164 |

| Harbour Residences West Coast, 2026 TOP |

Freehold, brand new | S$5,800,000 | ~S$1,742,600 | ~S$19,480 | ~S$35,418 |